July 28, 2022 17:01 ET | Source: Exco Technologies Ltd.

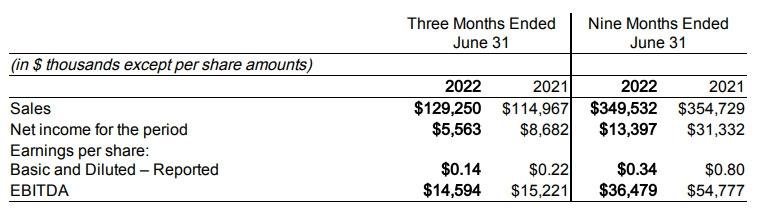

- Consolidated third quarter Sales of $129.2 million compared to $115.0 million in the prior year

- Net Income of $5.6 million and EPS of $0.14

- EBITDA of $14.6 million compared to $15.2 million in the prior year

- Halex Extrusion acquisition closed on May 2, 2022

- Growth capital expenditure strategy on track with $29.3 million in year-to-date spending

- Quarterly dividend of $0.105 per common share to be paid September, 30 2022

TORONTO, July 28, 2022 (GLOBE NEWSWIRE) — Exco Technologies Limited (TSX-XTC, OTCQX-EXCOF) today announced results for its third quarter of fiscal 2022 ended June 30, 2022. In addition, Exco announced a quarterly dividend of $0.105 per common share which will be paid on September 30, 2022 to shareholders of record on September 16, 2022. The dividend is an “eligible dividend” in accordance with the Income Tax Act of Canada.

“We continued to advance our aggressive growth agenda this quarter, completing the acquisition of Halex Extrusion Dies and making solid progress with our various capital projects”, said Darren Kirk, Exco’s President and CEO. “Our results demonstrate Exco’s ability to navigate through very challenging market conditions while benefiting from the electric vehicle revolution and worldwide movement towards reducing emissions”

Consolidated sales for the third quarter ended June 30, 2022 were $129.3 million compared to $115.0 million in the same quarter last year – an increase of $14.3 million, or 12%. Excluding foreign exchange rate movements, consolidated sales in the quarter were higher by 10% compared to the prior year and higher by 1% year-to-date.

The Automotive Solutions segment reported sales of $64.6 million in the third quarter – an increase of $3.6 million, or 6% from the prior year quarter. Excluding foreign exchange rate movements, segment revenues were higher by $2.6 million, or 4% for the quarter. Segment sales in the quarter were primarily influenced by vehicle production volumes in North American and Europe. IHS Markit estimates volumes increased 12% in North America and declined 5% in Europe compared to the prior year quarter. Segment sales were also negatively influenced by unfavorable vehicle mix, partially offset by ongoing key program launches for new and existing products as well as certain pricing actions taken to protect margins. While industry vehicle production volumes have shown some signs of improvement, they remain below the level of consumer demand due to supply chain disruptions (including the global semiconductor shortage), broad labour availability challenges, logistical constraints and ongoing COVID lockdown measures in China. European volumes are incrementally affected by localized supply chain challenges on that continent due to the Russian invasion of Ukraine. Nonetheless, HIS Markit expects North American and European production to grow through the second half of calendar 2022, which is expected to benefit segment results. Quoting opportunities have strengthened across the segment’s various businesses, which, together with new and ongoing product launches, are expected to support continued gains in Exco’s content per vehicle.

The Casting and Extrusion segment reported sales of $64.7 million for the third quarter – an increase of $10.7 million or 20%, from the same period last year. Foreign exchange rate changes increased sales $1.5 million in the quarter. The Company’s new European facilities (Halex) contributed $9.0 million of sales in the quarter, reflecting two months of activities. Demand for our extrusion tooling (ie dies, dummy blocks, stems, etc) and associated capital equipment (die ovens, containers, etc) remained strong due to both industry growth and ongoing market share gains. Demand for extrusion tools covers many industrial sectors including building and construction, large truck, electric vehicles, and many green energy sectors, all of which are focused on reducing energy intensity and reducing emissions. In anticipation of these trends intensifying, Exco has been increasing its manufacturing footprint in local markets in recent years including the acquisition of Halex in Europe. Management also remains focused on standardizing manufacturing processes, enhancing engineering depth and centralizing support functions across its various plants. These initiatives have reduced lead times, enhanced product quality, expanded product breadth and increased capacity, all of which has supported market share gains.

In the die-cast market, which primarily serves the automotive industry, demand has remained suppressed due to lower vehicle production volumes, which in turn, is due mainly to broader supply chain constraints. These constraints have been amplified by customer inventory destocking activity in recent quarters, particularly in the large mould segment, which has faced significantly lower rebuild work than typical. Demand and order flow for new moulds, associated tooling (shot sleeves, rods, rings, tips, etc) and even rebuild work however has recently picked up as industry vehicle production recovers and new electric vehicles and more efficient internal combustion engine/ transmission platforms are launched. In addition, demand for Exco’s industry leading additive (3D printed) tooling has continued to gain significant traction as customers focus on greater efficiency as the size and complexity of die cast tooling continues to increase. Sales in the quarter were also aided by price increases, which were implemented in order to protect margins from higher input costs. With respect to quoting activity, longer lead time items continue to see elevated demand for future activity (particularly large moulds) and inventories and backlog continue to grow which is expected to bode well for sales through the remainder of fiscal 2022 and into fiscal 2023.

Consolidated net income for the third quarter was $5.6 million or basic and diluted earnings of $0.14 per share compared to $8.7 million or $0.22 per share in the same quarter last year – a decrease of net income of $3.1 million. The consolidated effective income tax rate of 24% in the current quarter increased from 12% from the prior year. The change in income tax rate in the quarter was impacted by fiscal 2021 SRED tax credits booked in the third quarter last year, nondeductible losses from our Castool Morocco facility in fiscal 2022, geographic distribution, and foreign tax rate differentials

The Automotive Solutions segment reported pretax profit of $4.8 million in the third quarter a decrease of $0.3 million from the prior year quarter. The segment’s lower pretax profit was due to unfavorable market driven product mix changes, higher raw material, logistics and labour costs, the reversal of certain bad debt accruals last year, partially offset by certain pricing actions taken. Reduced industry vehicle production continued to cause inefficiencies within our operations. While customer orders and releases stabilized compared to prior quarters, sporadic and unreliable customer releases continued to impact production, increasing overhead and direct labour costs. These factors were intensified as we retained slack labour in anticipation of higher demand in the quarters ahead. Inflationary pressure continues to be a challenge in this segment particularly on petroleum-based products (resins, plastics, rubber), energy, freight and labour. Management remains focused on improving the efficiency of its operations and reducing its overall cost structure. Pricing discipline remains a focus and actions are being taken on current programs where possible, though there is typically a lag of a few quarters before the impact is realized. As well, new program awards are priced to reflect management’s expectations for higher future costs.

The Casting and Extrusion segment reported $4.8 million of pretax profit in the third quarter – a decrease of $3.0 million from the same quarter last year. The lower pretax profit was primarily driven by reduced activity for rebuild work in the Large Mould group coupled with shipments of new moulds. New mould programs can often have low to negative margins at the onset due to front-end inefficiencies that are improved as subsequent moulds are delivered. As well, profitability was negatively impacted by raw material and labour cost inflation, unfavorable market driven product mix shifts, reduced labour availability and higher overtime costs across the three business units. Start-up losses of Castool’s plant in Morocco (which opened in November 2021), and new heat treatment operations in Newmarket also negatively impacted profitability, mainly due to non-cash depreciation of plant and equipment. Segment pre-tax profitability however benefited from contributions from the acquisition of Halex and was higher sequentially for the second consecutive quarter. New business awards across the quarter remained very strong, particularly for structural die-cast components and those for electric vehicle platforms. The segment ended the quarter with backlogs approaching historic high levels. Management remains focused on taking pricing action where possible to preserve margins, reducing its overall cost structure and improving manufacturing efficiencies. Such activities together with sales efforts are expected to improve segment profitability in future quarters.

Consolidated EBITDA for the third quarter totaled $14.6 million compared to $15.2 million in the same quarter last year – a decrease of $0.6 million. For the quarter, EBITDA as a percentage of sales decreased to 11.3% in the current period compared to 13.2% the prior year driven by a reduction in segment margins in both the Casting & Extrusion segment (15% compared to 21%) and the Automotive Solutions segment (10% compared to 11%).

Exco generated cash from operating activities of $14.1 million during the quarter and $9.9 million of Free Cash Flow after $3.5 million in Maintenance Fixed Asset Additions. This cash flow, together with cash on hand was more than sufficient to fund fixed assets for growth initiatives of $12.0 million and $4.1 million of dividends. Exco utilized $60 million of its credit facility to fund its investment in Halex. The growth capital expenditure initiatives include: a) new Castool production facilities in Morocco and Mexico. The Moroccan facility opened in November 2021 and the Mexican facility which began construction in the second quarter. b) Investment in new heat treatment equipment in the tooling group to increase capacity, reduce emissions and enable us to in-source most of our requirements. c) Investments in the Large Mould group to upgrade its capabilities to handle moulds of extreme sizes which we expect will be increasingly demanded by most traditional and new OEMs. d) Investment in additional 3D printing machinery in our tooling group to meet strong customer demands. e) Expansion of two of our production facilities in the Automotive Solutions group to provide added capacity for awarded programs. Exco ended the quarter with $65 million in net indebtedness. The company has $33.9 million in available liquidity under its credit facility and $26.6 million of balance sheet cash, continuing its practice of maintaining a very strong balance sheet and liquidity position.

Outlook

Despite current macro-economic challenges, including tightening monetary conditions, the overall outlook is very favorable across Exco’s segments into the medium term. Consumer demand for automotive vehicles is currently outstripping supply in most markets, which are constrained by a shortage of semiconductor chips and, to a lesser extent, other raw materials, components and availability of labour. Dealer inventory levels are near record lows, while average transaction prices for both new and used vehicles are at record highs and the average age of the broader fleet has continued to increase to an all-time high. This bodes well for higher levels of future vehicle production and the sales opportunity of Exco’s various automotive components and accessories once supply chains normalize. In addition, OEM’s are increasingly looking to the sale of higher margin accessory products as a means to enhance their own levels of profitability. Exco’s Automotive Solutions segment derives a significant amount of activity from such products and is a leader in the prototyping, development and marketing of the same. Moreover, the rapid movement towards an electrified fleet for both passenger and commercial vehicles is enticing new market entrants into the automotive market while causing traditional OEM incumbents to further differentiate their product offerings, all of which is driving above average opportunities for Exco.

With respect to Exco’s Casting and Extrusion segment, the intensifying global focus on environmental sustainability is creating significant growth drivers that are expected to persist through at least the next decade. Automotive OEMs are looking to light-weight metals such as aluminum to reduce vehicle weight and reduce carbon dioxide emissions. This trend is evident regardless of powertrain design – whether internal combustion engines, electric vehicles or hybrids. As well, a renewed focus on the efficiency of OEMs in their own manufacturing process is creating higher demand for advanced tooling that can contribute towards their profitability and sustainability goals. Certain new EV manufacturers have adopted the approach of utilizing much larger die cast machines to cast entire sub-frames of vehicles out of an aluminum based alloy rather than assemble numerous pieces of separately stamped and welded pieces of ferrous metal. Exco expects traditional OEMs will ultimately follow this trend and is positioning its operations to capitalize accordingly. Beyond the automotive industry, Exco’s extrusion tooling supports diverse end markets which are also seeing increased demand for aluminum driven by environmental trends, including energy efficient buildings, solar panels, etc.

On the cost side, inflationary pressures have intensified in recent quarters while prompt availability of various input materials, components and labour has become more challenging. We are offsetting these dynamics through various efficiency initiatives and taking pricing action where possible although there is typically several quarters of lag before the counter measures are evident.

The Russian invasion of Ukraine has added additional uncertainty to the global economy in recent months. And while Exco has essentially no direct exposure to either of these countries, Ukraine does feed into the European automotive markets and Europe has significant dependence on Russia for its energy needs.

Exco itself is also looking inwards with respect to ESG and sustainability trends to ensure its own operations are sustainable. We are investing significant capital to improve the efficiency and capacity of our own operations while lowering our own carbon footprint. In the first quarter we released our first Sustainability Report on our corporate website which is available at: www.excocorp.com/leadership/sustainability/.

Exco is currently targeting a compounded average annual growth rate (excluding acquisitions) of approximately 10% for revenues and slightly higher levels for EBITDA and Net Income through fiscal 2026, which is expected to produce an annual EPS of roughly $1.90 by the end of this timeframe. This target is expected to be achieved through the launch of new programs, general market growth, and also market share gains consistent with the Company’s operating history. Capital investments will remain elevated in the balance of the fiscal year in order to position the Company for the significant growth opportunities we see. Capital expenditures are expected to exceed $55 million for fiscal 2022.

For further information and prior year comparison please refer to the Company’s Third Quarter Financial Statements in the Investor Relations section posted at www.excocorp.com. Alternatively, please refer to www.sedar.com.

Non-IFRS Measures: In this News Release, reference may be made to EBITDA, EBITDA Margin, Pretax Profit, Free Cash Flow and Maintenance Fixed Asset Additions which are not measures of financial performance under International Financial Reporting Standards (“IFRS”). Exco calculates EBITDA as earnings before interest, taxes, depreciation, amortization and other expenses and EBITDA Margin as EBITDA divided by sales. Exco calculates Pretax Profit as segmented earnings before other income/expense, interest and taxes. Free Cash is calculated as cash provided by operating activities less interest paid and Maintenance Fixed Asset Additions. Maintenance Fixed Asset Additions represents investment in fixed assets that are required to continue current capacity levels. EBITDA, EBITDA Margin, Pretax Profit and Free Cash Flow are used by management, from time to time, to facilitate period-to-period operating comparisons and we believe some investors and analysts use these measures as well when evaluating Exco’s financial performance. These measures, as calculated by Exco, do not have any standardized meaning prescribed by IFRS and are not necessarily comparable to similar measures presented by other issuers.

Quarterly Conference Call – July 29, 2022 at 10:30 a.m. (Toronto time):

To access the listen only live audio webcast, please log on to www.excocorp.com, or https://edge.media-server.com/mmc/p/x9fpqsmi a few minutes before the event. Those interested in participating in the question-and-answer conference call may register at https://register.vevent.com/register/BI3526160340204f7ea2ca7e205c624f44 to receive the dial-in numbers and unique PIN to access the call. It is recommended that you join 10 minutes prior to the event start (although you may register and dial in at any time during the call). For those unable to participate on July 29, 2022, an archived version will be available on the Exco website until August 13, 2022.

| Source: | Exco Technologies Limited (TSX-XTC) |

| Contact: | Darren Kirk, President and CEO |

| Telephone: | (905) 477-3065 Ext. 7233 |

| Website: | https://www.excocorp.com |

About Exco Technologies Limited:

Exco Technologies Limited is a global supplier of innovative technologies servicing the die-cast, extrusion and automotive industries. Through our 20 strategic locations in 9 countries, we employ approximately 5,000 people and service a diverse and broad customer base.

Notice To Reader: Forward Looking Statements

This press release contains forward-looking information and forward-looking statements within the meaning of applicable securities laws. We may use words such as “anticipate”, “may”, “will”, “should”, “expect”, “believe”, “estimate”, “5-year target” and similar expressions to identify forward-looking information and statements especially with respect to growth, outlook and financial performance of the Company’s business units, contribution of our start-up business units, contribution of awarded programs yet to be launched, margin performance, financial performance of acquisitions, liquidity, operating efficiencies, improvements in, expansion of and/or guidance or outlook as to future revenue, sales, production sales, margin, earnings, earnings per share, including the outlook for 2026, are forward-looking statements. These forward-looking statements include known and unknown risks, uncertainties, assumptions and other factors which may cause actual results or achievements to be materially different from those expressed or implied. These forward-looking statements are based on our plans, intentions or expectations which are based on, among other things, the current improving global economic recovery from the COVID-19 pandemic and containment of any future or similar outbreak of epidemic, pandemic, or contagious diseases that may emerge in the human population, which may have a material effect on how we and our customers operate our businesses and the duration and extent to which this will impact our future operating results, the impact of the Russian invasion of Ukraine on the global financial and automotive markets, including increased supply chain risks, assumptions about the number of automobiles produced in North America and Europe, production mix between passenger cars and trucks, the number of extrusion dies required in North America and South America, the rate of economic growth in North America, Europe and emerging market countries, investment by OEMs in drivetrain architecture and other initiatives intended to reduce fuel consumption and/or the weight of automobiles in response to rising climate risks, raw material prices, supply disruptions, economic conditions, inflation, currency fluctuations, trade restrictions, our ability to integrate acquisitions, our ability to continue increasing market share, or launch of new programs and the rate at which our current and future greenfield operations in Mexico and Morocco achieve sustained profitability. Readers are cautioned not to place undue reliance on forward-looking statements throughout this document and are also cautioned that the foregoing list of important factors is not exhaustive. The Company will update its disclosure upon publication of each fiscal quarter’s financial results and otherwise disclaims any obligations to update publicly or otherwise revise any such factors or any of the forward-looking information or statements contained herein to reflect subsequent information, events or developments, changes in risk factors or otherwise. For a more extensive discussion of Exco’s risks and uncertainties see the ‘Risks and Uncertainties’ section in our latest Annual Report, Annual Information Form (“AIF”) and other reports and securities filings made by the Company. This information is available at www.sedar.com or www.excocorp.com.